Double Entry Accounting

Introduction:

- Double entry accounting is the bedrock of modern financial management and reporting. Developed in the 15th century by Italian mathematician and Franciscan friar Luca Pacioli, this accounting method has stood the test of time and remains the cornerstone of financial systems worldwide. In this article, we will explore the fundamental principles of double entry accounting, its benefits, and its role in providing accurate and transparent financial information.

What is double entry accounting?

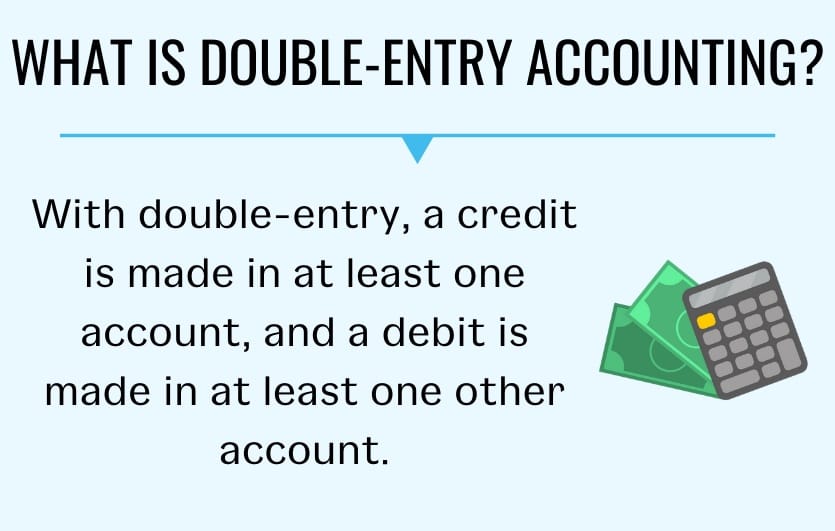

- Double entry accounting is a system where every financial transaction affects at least two accounts, with equal debits and credits. It ensures the accounting equation stays balanced, providing accurate and transparent financial records. This method, established by Luca Pacioli in the 15th century, is fundamental to modern financial management.

I. Understanding Double Entry Accounting:

The Basic Principle:

- At its core, double entry accounting is based on the principle that every financial transaction has two equal and opposite effects. For every debit entry, there must be a corresponding credit entry, ensuring that the accounting equation (Assets = Liabilities + Equity) always holds true.

Debits and Credits:

- Debits and credits are the two sides of every accounting entry. Understanding which accounts increase or decrease with each entry is crucial. Assets and expenses increase with debits, while liabilities, equity, and revenue increase with credits.

The Accounting Equation:

- The accounting equation forms the foundation of double entry accounting. It ensures that the balance sheet remains balanced by representing the financial position of a business at any given point in time.

II. The Process of Double Entry Accounting:

Recording Transactions:

- Every financial transaction involves the transfer of value between two accounts. For example, when a business makes a sale, it records a debit to cash or accounts receivable and a credit to revenue.

T-Accounts:

- T-accounts are a visual representation of the double entry system. They illustrate the flow of debits and credits to specific accounts, providing a clear picture of the impact of each transaction.

Journal Entries:

- Journal entries are the primary tool for recording transactions in double entry accounting. These entries are then transferred to the general ledger, summarizing all financial transactions in one central location.

III. Benefits of Double Entry Accounting:

Accuracy and Error Detection:

- The dual recording system helps identify errors quickly. If the books don't balance, accountants know there is a mistake that needs to be rectified.

Financial Reporting:

- Double entry accounting provides a solid foundation for creating accurate and reliable financial statements, such as the income statement, balance sheet, and cash flow statement.

Decision-Making:

- Businesses use double entry accounting to make informed decisions based on their financial position. It allows for a comprehensive analysis of income, expenses, assets, and liabilities.

IV. Double Entry Accounting in the Digital Age:

Accounting Software:

- With the advent of technology, accounting software has automated much of the double entry process. This has increased efficiency, reduced errors, and allowed for real-time financial reporting.

Integration with Business Operations:

- Modern accounting systems seamlessly integrate with other business operations, providing a holistic view of a company's financial health. This integration facilitates better decision-making and strategic planning.

Conclusion:

- Double entry accounting has proven to be a robust and reliable method for recording financial transactions. Its principles continue to guide accountants and businesses in maintaining accurate financial records, promoting transparency, and supporting informed decision-making. As technology continues to evolve, the core principles of double entry accounting remain essential for the financial well-being of organizations worldwide.

Also Read Our More Article:-

- Single Entry Accounting

- Understanding Bahi Khata: A Simple Guide to its Features

- How to Use Bahi Khata App?

- Cashbook Bahi Khata: Simplifying Financial Record-keeping for Small Businesses

- Significance of Credit Bahi Khata in Financial Management

Frequently asked question:

What is mean by double-entry in accounting?

- Double entry accounting is a system where every financial transaction affects at least two accounts, with equal debits and credits. It ensures the accounting equation stays balanced, providing accurate and transparent financial records. This method, established by Luca Pacioli in the 15th century, is fundamental to modern financial management.

What is the main rule for double-entry accounting?

- The main rule in double-entry accounting is that for every debit entry made to an account, there must be an equal and corresponding credit entry. This principle ensures that the accounting equation (Assets = Liabilities + Equity) remains balanced, providing a reliable framework for recording and reporting financial transactions.

Is double-entry debit or credit?

- In double-entry accounting, debits and credits are equal and opposite entries. Debits increase assets and expenses, while credits increase liabilities, equity, and revenue.

What is a T-account?

- A T-account is a visual representation used in accounting to illustrate the flow of debits and credits for a specific account. It helps organize and understand individual transactions.

What is double entry in accounting terms?

- In double-entry accounting, every transaction is recorded with debits and credits, representing the two sides of the entry. Debits are recorded on the left-hand side of the ledger and will:

- Increase asset and expense accounts

- Decrease revenue, equity, and liability accounts

This system ensures that the accounting equation stays balanced.

We hope that you like this content and for more such content Please follow us on our social site and YouTube and subscribe to our website.

Manage your business cash flows and payable/receivables using our Bahi Khata App.

Comments ()